2018 Federal Government Shutdown

What a Government Shutdown Means for REALTORS®

Congress has failed to approve a Continuing Resolution (CR) providing funding for most government operations. Therefore, spending authority for most of the government expired at midnight on January 19, 2018. Until legislation providing for funding is signed into law, many offices and programs of the federal government are now shut down. This means many, but not all, government programs, including some that impact federal housing and mortgage programs, have been suspended or slowed due to the lapse in government funding. The Office of Management and Budget (OMB) requires each agency to have contingency plans in place. The information below is based on NAR staff review of agency contingency plans for the current shutdown and past experience with previous shutdowns and near-shutdowns.

NFIP National Flood Insurance Program

An extension of the National Flood Insurance Program (NFIP) was attached to the CR that Congress failed to pass. This means that for the duration of the shutdown, the NFIP will not be able to issue new or renew flood insurance policies. However, existing policies will not be affected until 30 days after their expiration date. Homebuyers will also be able to assume existing policies and claims will continue to be processed and paid as usual. For more detailed information, FEMA’s latest guidance to insurance companies can be found here(link is external).

Federal Housing Administration

HUD’s Contingency Plan states that FHA will endorse new loans in the Single Family Mortgage Loan Program except for HECM loans. It will not make new commitments in the Multi-family Program during the shutdown. FHA will maintain operational activities including paying claims and collecting premiums. FHA Contractors managing the REO/HUD Homes portfolio can continue to operate. Loss mitigation programs will continue to operate. You can expect some delays with FHA processing due to short staffing. (See the HUD Contingency Plan for Possible Lapse in Appropriations(link is external) for more info.)

Government Sponsored Enterprises

During previous shutdowns, Fannie Mae and Freddie Mac have continued normal operations, just as their regulator, the Federal Housing Finance Agency, since they are not reliant on appropriated funds. Fannie and Freddie are expected to announce relaxed procedures that would permit closings to go forward without federal verification of Social Security numbers and IRS tax transcripts. However, lenders would still have to obtain federal verification of both before the GSE’s will accept loans for purchase. Any relaxed requirements would not apply to loan modification re-financings.

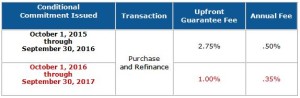

Rural Housing Programs

The U.S. Department of Agriculture will not issue new rural housing Direct Loans or Guaranteed Loans. Scheduled closings of Direct Loans will not occur. Scheduled closings of Guaranteed Loans without the guarantee previously issued would be closed at the lender’s own risk.

VA Loan Guaranty Program

The VA loan guaranty program will be operational. The VA has determined that housing is an “essential service.” In addition, VA projects that “95.5% of VA employees would either be fully funded or required to perform excepted functions during a shutdown” (Download the VA Contingency Plan here(link is external) for more info.)

Internal Revenue Service

The IRS is closed and has suspended the processing of all forms, including requests for tax return transcripts (Form 4506T). While FHA and VA do not require these transcripts, they are required by many lenders for many kinds of loans, including FHA and VA, so delays can be expected if the shutdown is protracted. We have received indications that many loan originators are adopting revised policies during the shutdown, such as allowing for processing and closings with income verification to follow, as long as the borrower has signed a Form 4506T requesting IRS tax transcripts. On loans requiring a Form 4506T Fannie Mae and Freddie Mac are expected to adopt relaxed provisions allowing closings but subject to tax transcript verification before the GSE’s purchase the loans.

Social Security Administration

The Social Security Administration is closed and has suspended most customer service functions. According to the SSA Contingency Plan, verifying Social Security numbers through the Consent Based SSN Verification Service will also be suspended during the shutdown, a further complication for mortgage processing. As with IRS income verification, policies vary among lenders, with many choosing to exercise forbearance during the shutdown period subject to subsequent verification. Fannie Mae and Freddie Mac are expected to adopt policies to allow for closing subject to subsequent verification and before GSE purchase of the loan.

For more information contact:

Dean Henderson, CRMS

(661)726-9000

{kind=link}